Why Whole Life Outperforms Savings Accounts Long Term

- Jib Hunt

- 1 day ago

- 8 min read

COMPLIANCE NOTE: For educational purposes only. Not financial, tax, or legal advice.

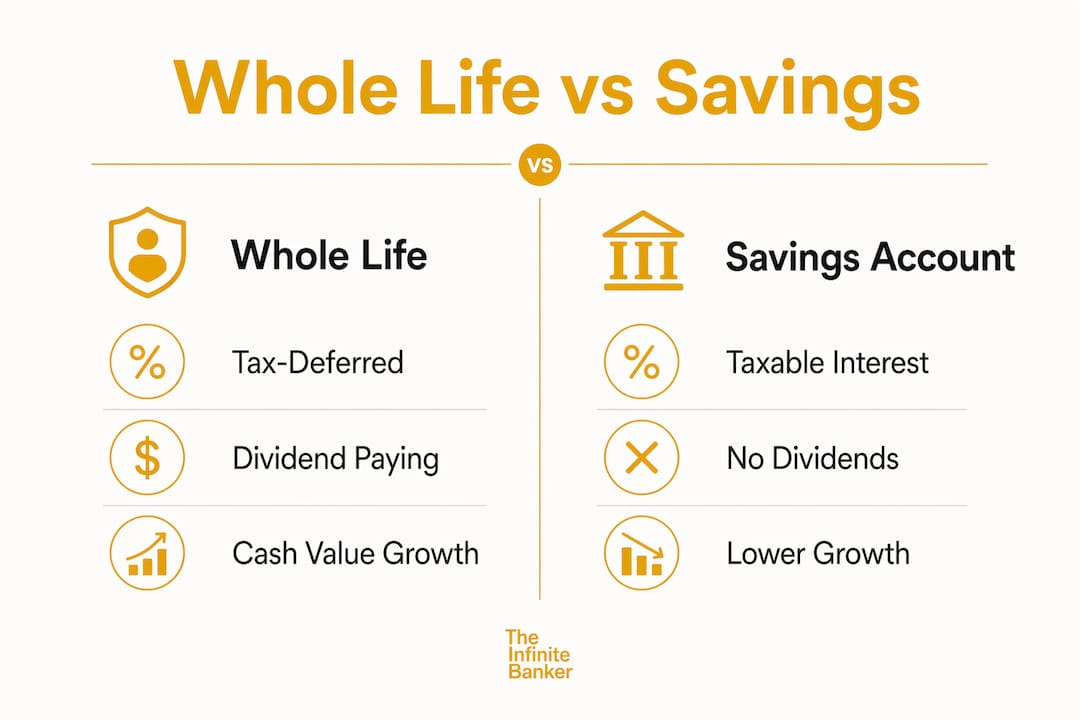

Whole life insurance is a permanent life insurance policy that combines a death benefit with a tax-deferred cash value component, offering features a standard savings account cannot match. The industry term for this strategy is dividend-paying whole life insurance, and it sits at the center of what practitioners call the Infinite Banking Concept. A savings account provides liquidity and FDIC protection, but it generates taxable interest, carries no death benefit, and offers limited asset protection. Whole life insurance addresses all three gaps at once, which is why whole life outperforms savings accounts as a long-term financial tool for entrepreneurs, investors, and high-income earners who need more than a place to park cash.

Why whole life outperforms savings accounts in cash value growth

Cash value inside a whole life policy grows tax-deferred, meaning you owe no annual income tax on the accumulation. A savings account earns interest that the IRS taxes in the year it is credited. That annual tax drag compounds against you over time, reducing the net growth rate of every dollar sitting in a bank account.

Dividend-paying whole life policies issued by mutual insurers add another layer of growth potential. Many mutual insurers have paid dividends consistently for decades, though dividends are never guaranteed. When those dividends are applied as paid-up additions (PUAs), they purchase additional increments of paid-up insurance, which in turn generate their own cash value and future dividends. The Paid-Up Additions rider is the engine of this compounding effect.

Well-structured policies designed to favor cash accumulation over death benefit size can achieve internal rates of return in the range of 3.5% to 5% after the early funding years. That range is not spectacular on paper, but it is net of insurance costs, tax-deferred, and attached to a death benefit. A savings account or money market fund offering a similar nominal rate still loses ground once you account for annual taxation.

Feature | Whole life insurance | Standard savings account |

Tax treatment on growth | Tax-deferred | Taxable annually |

Death benefit | Yes, income tax-free to beneficiaries | None |

Dividend potential | Yes, not guaranteed | No |

Creditor protection | Varies by state, generally strong | Limited |

Liquidity method | Policy loans or withdrawals | Direct withdrawal |

Pro Tip: Ask any insurer for an illustration showing the internal rate of return on cash value at years 10, 20, and 30. That single number cuts through marketing language and lets you compare policies on equal footing.

What financial protections does whole life offer that savings accounts lack?

Whole life insurance carries a set of protections that savings accounts simply do not provide. Understanding them clarifies why the comparison goes beyond interest rates.

Income tax-free death benefit. Death benefits are generally income tax-free to named beneficiaries and can bypass probate entirely, unlike a savings account balance that passes through the estate. That distinction matters for legacy planning.

Creditor protection. Cash value enjoys stronger creditor protection than bank accounts in most states. The specific rules vary by state, but many states exempt life insurance cash value from creditor claims entirely. A savings account has no equivalent shield.

Policy loan access without a taxable event. Loans taken against cash value are generally not treated as taxable income when the policy is properly structured and maintained. This creates a liquidity mechanism that does not trigger a tax bill the way a withdrawal from a taxable account would. Policy loans do accrue interest and reduce both cash value and the death benefit if left unpaid, so careful management is required.

No income phase-outs. Contributions to a whole life policy are not subject to the income limits that restrict Roth IRA or 401(k) contributions. High earners who are phased out of traditional retirement vehicles can still fund a whole life policy without restriction.

Permanent coverage. A savings account can be closed or depleted. A properly funded whole life policy remains in force for life, providing a guaranteed death benefit regardless of health changes after issue.

Common misconceptions about whole life vs. savings accounts

The most persistent misconception is that whole life insurance is a direct substitute for equity investing. It is not. Whole life is a capital base, not a growth engine. Treating it as a stock-market alternative sets up unrealistic expectations and leads to poor policy decisions.

A second misconception involves cost. High initial premiums and commission structures cause slow cash value growth in the early years, and returns can be negative in year one or two. This is not a flaw unique to whole life. It is the cost of acquiring permanent insurance coverage and a long-term financial asset. The math improves substantially over a 10-to-20-year horizon.

A third misconception is that all whole life policies are the same. Policy design matters enormously. Commission structures often skew standard policy designs toward maximizing the death benefit rather than cash accumulation. A policy built for an agent’s commission is not the same as one built for your capital efficiency. The most effective policies for cash accumulation use a minimal base death benefit combined with a maximized Paid-Up Additions rider, issued by a mutual insurer with a consistent dividend history.

Here is a practical framework for evaluating whether whole life fits your financial plan:

Define the purpose. Whole life works best as a long-term capital reserve, a liquidity buffer, or a legacy tool. If you need the money within five years, a savings account is the better choice.

Verify the policy design. Confirm the illustration shows a high PUA allocation relative to the base premium. A low PUA ratio signals a commission-heavy design.

Check the insurer’s dividend history. Mutual insurers with decades of consecutive dividend payments offer more predictable long-term performance, though past dividends do not guarantee future ones.

Model the after-tax comparison. Compare the whole life internal rate of return against the after-tax yield on savings accounts or bonds at your marginal tax rate.

Plan for the long term. Whole life requires a commitment of at least 10 years to overcome early costs. Entering without that horizon is the primary reason policyholders surrender policies at a loss.

Pro Tip: Run a side-by-side illustration comparing a savings account earning a competitive rate, taxed at your marginal rate, against the whole life internal rate of return over 20 years. The after-tax gap is almost always larger than you expect.

How does whole life fit into a broader financial plan?

Whole life insurance functions as a non-correlated buffer asset within a diversified portfolio. Its cash value does not fluctuate with equity markets, which means it holds its value during bear markets when other assets are declining.

This stability has a measurable portfolio effect. Including whole life insurance in a retirement portfolio shifts the efficient frontier, allowing an investor to hold a higher equity allocation elsewhere without increasing overall sequence-of-returns risk. That is a meaningful advantage for anyone approaching retirement who wants growth without the full volatility of an all-equity portfolio.

Whole life also provides a practical liquidity solution during market downturns. Rather than selling equities at depressed prices to cover living expenses or business capital needs, you can borrow against cash value and repay the loan when markets recover. This approach preserves the compounding trajectory of your equity holdings. Policy loans accrue interest and reduce the death benefit if unpaid, so this strategy requires active management.

Whole life can supplement or partially replace fixed-income allocations for investors who want tax-deferred growth with lower volatility.

It supports legacy planning by passing a death benefit directly to named beneficiaries, bypassing probate.

It provides a capital reserve for entrepreneurs who need access to funds for business opportunities without liquidating investments.

Traditional savings accounts remain the better choice for short-term liquidity needs, emergency funds, and goals with a horizon under five years.

The key distinction is purpose. Whole life is not a replacement for all savings. It is a complementary tool that performs specific functions a savings account or bond portfolio cannot replicate.

Key Takeaways

Dividend-paying whole life insurance outperforms savings accounts over the long term because it combines tax-deferred cash value growth, creditor protection, a death benefit, and portfolio diversification benefits that no bank account can provide.

Point | Details |

Tax-deferred growth advantage | Cash value grows without annual taxation, unlike savings account interest which is taxed each year. |

Policy design determines returns | A high Paid-Up Additions rider allocation is the primary driver of strong cash value accumulation. |

Creditor and estate protections | Cash value carries state-level creditor protection and death benefits bypass probate for beneficiaries. |

Portfolio buffer function | Whole life acts as a non-correlated asset that can reduce sequence-of-returns risk in retirement. |

Long-term commitment required | Early costs make whole life inefficient under a 10-year horizon; the math improves substantially over time. |

My honest view on whole life as a financial tool

I have worked with entrepreneurs and investors who came to whole life insurance after years of parking capital in savings accounts and money market funds, wondering why their liquid reserves were not working harder. The honest answer is that savings accounts are designed for safety and access, not for capital efficiency. Whole life, when structured correctly, is a different category of asset entirely.

The part most people miss is the policy design conversation. The difference between a policy built for an agent’s commission and one built for your capital efficiency is not subtle. It shows up in the illustration numbers within the first three years. If a policy is not showing meaningful cash value by year three, the design is probably wrong for accumulation purposes.

What I find most compelling about properly structured whole life is its role as a liquidity reserve that does not require you to sell anything. During the 2022 equity drawdown, investors who held whole life policies could access capital through policy loans without triggering a taxable event or locking in losses. That is a real, practical advantage that a savings account cannot replicate in a portfolio context.

Whole life is not for everyone. If you need your money within five years, or if you are not in a position to commit to a multi-decade premium schedule, a savings account or short-term bond ladder is the right tool. But for high-income earners building a long-term financial structure, whole life deserves a serious look as a capital base, not a replacement for equities or savings, but a complement to both.

— Jib Hunt, Authorized IBC Practitioner

How The Infinite Banker approaches whole life strategy

The Infinite Banker works with entrepreneurs, real estate investors, and high-income earners who want to put their capital to work more efficiently than a savings account allows.

The focus is on properly structured dividend-paying whole life insurance policies designed for capital accumulation, not just death benefit coverage. Every strategy starts with policy design, because a poorly structured policy undermines the entire financial case for whole life. If you are evaluating how whole life insurance may fit your financial plan, The Infinite Banker provides resources, illustrations, and access to Authorized IBC Practitioners who can walk you through the numbers without the sales pressure. The goal is clarity, not a quick close.

FAQ

What makes whole life insurance better than a savings account?

Whole life insurance offers tax-deferred cash value growth, a death benefit, and creditor protection that savings accounts do not provide. Over a long horizon, the after-tax growth advantage and added protections make it a more efficient capital vehicle for high-income earners.

Are whole life dividends guaranteed?

Whole life dividends are not guaranteed. Many mutual insurers have paid them consistently for decades, but past performance does not obligate future payments. Policy illustrations that assume dividends should be read as projections, not promises.

Can I access cash value without paying taxes?

Policy loans against whole life cash value are generally not treated as taxable income when the policy is properly structured and maintained. Unpaid loans accrue interest and reduce both cash value and the death benefit, and a lapsed policy can trigger a taxable event.

How does whole life compare to bonds in a portfolio?

Whole life insurance can serve a similar stabilizing role as fixed-income allocations, but with tax-deferred growth and a death benefit that bonds do not carry. Research indicates it can shift the efficient frontier in a retirement portfolio, allowing higher equity exposure without proportionally higher risk.

When does a savings account make more sense than whole life?

A savings account is the better choice for emergency funds, short-term goals, and any capital you may need within five years. Whole life’s early costs make it inefficient for short horizons, and it requires a long-term commitment to deliver its full financial benefits.

This post is educational only and not financial, tax, or legal advice. Consult qualified professionals before acting.