Whole Life Insurance in Your Real Estate Portfolio

- Jib Hunt

- 4 days ago

- 9 min read

Updated: 3 days ago

COMPLIANCE NOTE: For educational purposes only. Not financial, tax, or legal advice.

Whole life insurance is a permanent financial tool that builds guaranteed cash value, provides tax-free access to capital, and creates liquidity for estate obligations without forcing property sales. The role of whole life in a real estate portfolio goes well beyond death benefit coverage. Properly structured dividend-paying whole life policies function as a private capital reserve, an estate planning instrument, and a tax-advantaged bond substitute, all within a single contract. The Infinite Banker works with real estate investors to implement these structures for long-term capital efficiency and financial control.

How does whole life insurance support real estate financing?

Whole life insurance builds cash value that grows on a guaranteed basis, unaffected by stock market swings. Cash value grows through dividends that compound over time, creating a private reserve you can access without selling an asset or qualifying for a bank loan. That characteristic makes it a uniquely flexible financing tool for real estate investors who need capital on short notice.

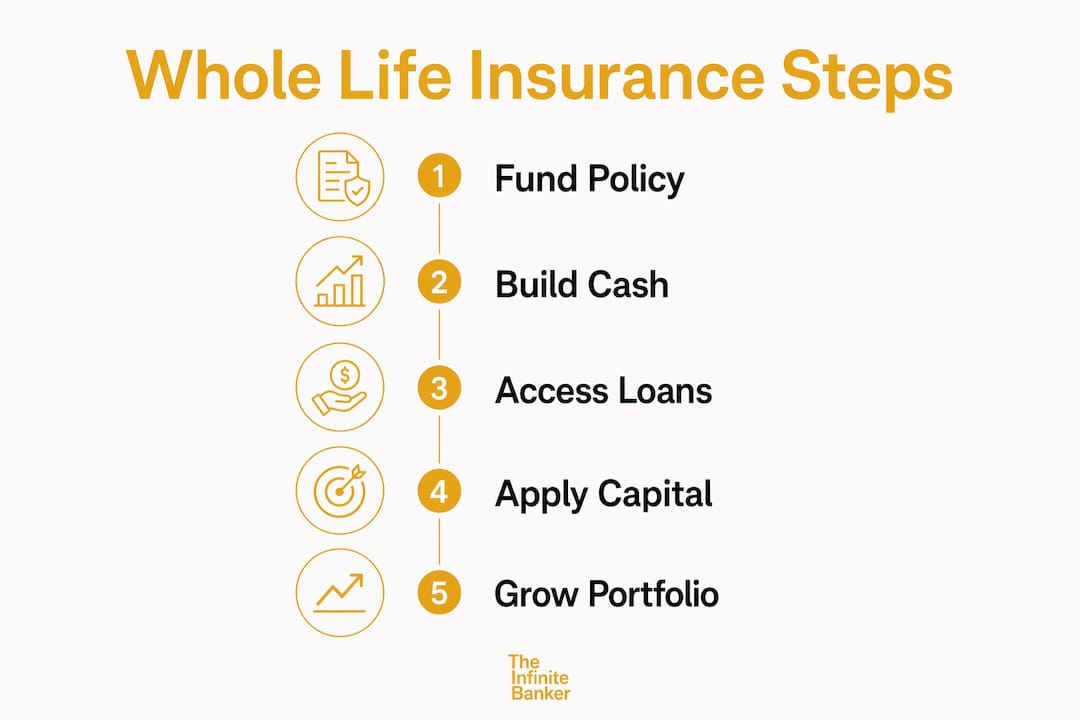

The Infinite Banking Concept formalizes this approach. You fund a whole life policy, build cash value, then borrow against it to fund down payments, bridge financing gaps, or cover renovation costs. The policy loan is not a taxable event when the policy is correctly structured. Your cash value continues to earn dividends even while the loan is outstanding, which means your capital is effectively working in two places at once.

Policies overfunded near the Modified Endowment Contract limit with a paid-up additions rider build cash value faster than standard designs. Accessing cash value through policy loans is tax-free and functions similarly to a Roth IRA but without contribution limits or income phase-outs. That distinction matters for high-income real estate investors who have already maxed out traditional tax-sheltered accounts.

Key ways cash value supports real estate financing:

Down payment capital. Policy loans provide a ready source of funds for property acquisitions without triggering a taxable withdrawal.

Bridge financing. When a deal closes before a sale completes, cash value covers the gap without bank approval timelines.

Renovation reserves. Investors hold cash value as a liquid reserve for capital expenditures rather than keeping idle cash in low-yield accounts.

Debt service coverage. During vacancy periods, policy loans can cover mortgage payments without disrupting the portfolio.

Pro Tip: Design your policy with a paid-up additions rider and fund it as close to the Modified Endowment Contract limit as possible. This maximizes early cash value growth and reduces the funding lag that frustrates investors who expect immediate liquidity.

What is trust-owned life insurance and why does it matter?

Trust-owned life insurance, commonly called TOLI, is a structure where an irrevocable trust owns and is the beneficiary of a whole life policy. This arrangement removes the death benefit from the insured’s taxable estate while preserving the family’s ability to access proceeds for estate taxes and debt repayment. For real estate investors with significant property holdings, this distinction is the difference between heirs keeping the portfolio intact and being forced to sell properties to cover tax bills.

Spousal Lifetime Access Trusts can hold policies worth over $30 million while keeping proceeds outside the taxable estate. A Spousal Lifetime Access Trust, or SLAT, allows the insured’s spouse to receive distributions from the trust during their lifetime, maintaining practical access to the capital while the death benefit avoids estate taxation. That combination of asset protection and access is difficult to replicate with any other financial instrument.

Here is how TOLI integrates with real estate estate planning:

Establish the trust. Work with an estate planning attorney to create an irrevocable trust structured for your state’s laws and your family’s goals.

Fund the policy. The trust purchases a whole life policy on the investor’s life. Premiums are funded through annual gifts to the trust, often using the annual gift tax exclusion.

Accumulate cash value. The policy builds cash value inside the trust, available for trust distributions or policy loans if the trust document permits.

Deploy the death benefit. At death, proceeds pass to the trust income-tax-free and are used to pay estate taxes, retire property debt, or distribute to heirs without a forced sale.

Trust-owned life insurance preserves real estate ownership by providing tax-free death benefits that pay estate taxes and debts, eliminating the need to liquidate properties under pressure. Investors also maintain operational control and financing flexibility because the properties themselves remain in the investor’s name or operating entities.

Estate Planning Tool | Estate Tax Exposure | Forced Sale Risk | Liquidity Source |

No life insurance | High | High | Property sale |

Term life insurance | Moderate | Moderate | Temporary death benefit |

TOLI with SLAT structure | Low | Low | Tax-free death benefit |

Pro Tip: Coordinate your TOLI structure with both an estate planning attorney and a policy design specialist. A policy that is correctly funded but placed in a poorly drafted trust can still trigger inclusion in the taxable estate.

How does whole life compare to other real estate financing tools?

Whole life insurance is not a replacement for mortgage financing or traditional investment accounts. It is a stabilizing layer that complements those tools and fills gaps they cannot address. Combining whole life insurance with investments and annuities often yields more retirement income and a larger legacy than investments alone. That outcome reflects the tax efficiency and permanence that whole life adds to a portfolio.

Term life insurance costs less in the short term but provides no cash value and expires. A real estate investor who relies on term coverage has no living benefit, no capital reserve, and no estate liquidity mechanism beyond the policy’s expiration date. Term life is temporary with no cash value, while whole life’s permanent coverage includes living benefits that enhance portfolio diversification. The cost difference between term and whole life is real, but so is the functional difference.

Whole life policies designed with maximum paid-up additions and minimized death benefit produce returns that compete with taxable bonds on an after-tax basis. Selecting low-load carriers and avoiding commission-heavy structures improves the internal rate of return and tax efficiency of the policy. For investors in high federal and state tax brackets, that tax efficiency compounds significantly over a 20-year or 30-year holding period.

Key advantages whole life holds over conventional financing tools:

No credit qualification. Policy loans do not require income verification, debt-to-income analysis, or lender approval.

No repayment schedule. Loan repayment is flexible. You set the pace, which protects cash flow during slow rental periods.

Tax-free access. Policy loans are not reported as income, unlike withdrawals from traditional retirement accounts.

Market independence. Cash value does not decline during recessions, making it available precisely when other capital sources contract.

Practical steps for integrating whole life into your investment strategy

Policy design is the first decision and the most consequential one. A whole life policy structured for maximum death benefit and minimum cash value serves a different purpose than one structured for maximum early cash value. Real estate investors need the latter. Work with a specialist who understands the Infinite Banking Concept and can design a policy near the Modified Endowment Contract limit with a substantial paid-up additions rider.

Premium funding strategy determines how quickly cash value becomes usable. Front-loading premiums in the early years accelerates accumulation and shortens the funding lag. Over decades, cash values can accumulate to $600,000 or $700,000 or more, accessible without reported income if the policy remains in force. That scale of tax-free capital is a material asset in any real estate portfolio.

Managing policy loans requires discipline. Treat outstanding loans as real debt with a repayment plan. Loans left unpaid reduce the death benefit and, if the policy lapses with a large outstanding loan, can trigger a taxable event. Coordinate loan activity with your accountant and policy administrator to avoid unintended tax consequences.

Common pitfalls to avoid:

Underfunding the policy. Paying only the base premium produces slow cash value growth and limits the policy’s usefulness as a capital tool.

Ignoring the carrier’s financial strength. Dividend-paying whole life policies depend on the carrier’s long-term financial health. Choose a mutual insurance company with a consistent dividend history.

Treating policy loans as free money. Loans accrue interest. Unmanaged loan balances erode cash value and can destabilize the policy.

Misaligning policy design with investment timeline. A policy designed for a 30-year horizon performs differently than one designed for a 10-year exit. Match the design to your actual investment plan.

Pro Tip: Ask your policy specialist for an in-force illustration showing projected cash value at years 5, 10, 15, and 20 under both the guaranteed and dividend scenarios. That illustration is your planning baseline, not a sales document.

Key Takeaways

Whole life insurance functions as a permanent capital reserve, estate planning tool, and tax-efficient bond substitute that strengthens a real estate portfolio across every stage of the investment lifecycle.

Point | Details |

Cash value as capital reserve | Policy loans provide tax-free, credit-free capital for down payments, bridge financing, and renovation costs. |

TOLI for estate protection | Trust-owned policies keep death benefits outside the taxable estate, preventing forced property sales at death. |

Policy design determines results | Maximizing paid-up additions and funding near the MEC limit accelerates cash value and improves tax efficiency. |

Whole life complements, not replaces | Whole life works alongside mortgage financing and investment accounts, not as a substitute for them. |

Loan discipline is non-negotiable | Unmanaged policy loans reduce death benefit and can trigger taxable events if the policy lapses. |

What I’ve learned from watching investors use whole life the wrong way

The most common mistake I see is investors treating a whole life policy as a savings account they can raid without consequence. They borrow heavily in the early years, pay nothing back, and then wonder why their cash value has stalled. The policy loan mechanism is powerful precisely because it is flexible. That flexibility requires more discipline, not less.

The second mistake is buying a policy designed for death benefit rather than cash value accumulation. A real estate investor does not need a $5 million death benefit in year one. They need $200,000 in accessible cash value by year three. Those are different policy designs, and most general insurance agents will not know the difference. Working with a specialist who understands infinite banking for real estate investors changes the outcome materially.

What I find genuinely underappreciated is the estate planning dimension. Investors spend years building a portfolio worth $10 million or $20 million and give almost no thought to what happens at death. A TOLI structure with a SLAT can protect that portfolio from estate taxes and forced liquidation at a fraction of the cost of losing it. The investors who implement this early, before the estate grows beyond exemption limits, are the ones whose families actually keep the portfolio intact.

My recommendation is straightforward. Treat whole life as a financial infrastructure decision, not a product purchase. Get the policy design right, fund it consistently, manage loans with intention, and coordinate the structure with your estate plan. Done correctly, it becomes one of the most durable assets in your portfolio.

— Jib Hunt

How The Infinite Banker approaches whole life for real estate investors

Real estate investors who want to put whole life insurance to work in their portfolios need more than a policy. They need a structure designed around their capital cycle, their tax situation, and their long-term exit plan.

The Infinite Banker specializes in exactly that. The firm works with real estate investors and high-income earners to design dividend-paying whole life policies built for capital efficiency, not just coverage. From policy design and premium structuring to coordinating with estate planning attorneys, The Infinite Banker provides the guidance that turns a whole life policy into a functioning part of your investment infrastructure. If you are ready to build a personal banking system around your real estate portfolio, The Infinite Banker is the place to start.

FAQ

What is the role of whole life in a real estate portfolio?

Whole life insurance builds guaranteed cash value that investors can access through policy loans to fund acquisitions, cover expenses, and provide estate liquidity without selling properties. It functions as a private capital reserve and estate planning tool within a real estate investment strategy.

How does the Infinite Banking Concept apply to real estate?

The Infinite Banking Concept uses a dividend-paying whole life policy as a personal banking system. Real estate investors borrow against their cash value to fund deals, then repay the loan on their own schedule, keeping capital working continuously.

What is trust-owned life insurance and how does it protect a portfolio?

Trust-owned life insurance places a whole life policy inside an irrevocable trust, removing the death benefit from the taxable estate. At death, proceeds pay estate taxes and debts, preventing heirs from being forced to sell properties to cover those obligations.

Are policy loans from whole life insurance taxable?

Policy loans are not taxable events when the policy is correctly structured and remains in force. The loan is treated as a debt against the policy, not a distribution, so no income is reported to the IRS.

How is whole life different from term life for real estate investors?

Term life is temporary and builds no cash value, making it useful only as a death benefit for a fixed period. Whole life is permanent, accumulates cash value, and provides living benefits that real estate investors can use during their lifetime for financing and estate planning.

This post is for educational purposes only and does not constitute financial, tax, or legal advice. Individual circumstances vary. Consult with qualified professionals before making any decisions regarding insurance or capital strategy.